Risky and reckless: Bronson wants to double Perm Fund earnings

Former Anchorage Mayor Dave Bronson, one of the legions of Republican candidates for governor, says he wants to more than double the earnings of the Alaska Permanent Fund to pay higher dividends, avoid new taxes and solve the state’s financial woes.

Bronson and his running mate, Fairbanksan Josh Church, may be newcomers to state politics, but that doesn’t excuse this cavalier manner of trying to inject their politics into the fund’s management.

This is a new wrinkle on the “no tax” blather that Mike Dunleavy rode to victory in 2018 and 2022, a con game that most Republican candidates seem to be pursuing in hopes they will fool just enough voters in 2026.

The last thing we need is a governor dictating that the fund should be earning 12 percent to 14 percent, not the 5 percent above inflation target it has had for many years.

The Bronson investment plan is a recipe for disaster.

But it’s also a great reminder of why the Alaska Legislature needs to address the shortcomings in the current management of the Permanent Fund.

As it stands now, any governor could do what Bronson is proposing and force the Alaska Permanent Fund Corporation to change its investment strategy and take on much higher risks to try to earn more money. An approach that can also lead the corporation to lose a lot of money.

Withing two years of a gubernatorial election, the state’s chief executive can have a working majority of the six trustees, who can be chosen with the understanding that they will do what the governor demands—even if it means taking on enormous new risks that have not been explained to the public.

With the lack of Permanent Fund oversight by the Legislature, a 40-year tradition, there is nothing stopping the next governor from forcing the trustees to overhaul the fund’s management and take more risks. The prudent investor rule is supposed to apply to the fund, but the danger is that anything the governor wants will be defined as prudent.

If an investment target of 5 percent above inflation is too conservative for Alaska’s most important financial institution, we need a complete examination and a public discussion of whether greater risk is acceptable.

Here is the campaign document from Bronson and Church, in which they say the target investment return rate should be 10 percent. They don’t justify this number or say how it would be attained.

In a recent gubernatorial debate, Bronson said he wanted the fund to earn 12 percent to 14 percent a year. Perhaps he meant that adjusted for inflation there would be a real growth rate of 10 percent.

In either case, his use of conflicting numbers does not inspire confidence in his conflicting numbers.

He falsely claimed that the state’s fiscal situation is because politicians “grew government to the point where we can’t” pay a full PFD. He failed to mention the two largest factors—lower oil production and lower oil taxes.

The state can’t pay a full dividend under the law right now, but it could in the future without new taxes, according to Bronson’s dream.

He said, “the good news is there’s a way out of it. So about 30 percent of our budget is oil. The other 70 percent is earnings off the Permanent Fund. We need to grow. We’re getting terrible, we’re like a C student on our returns on the Permanent Fund. We need, if we’re an A student and we can get it up to 12 or 14 percent.”

With 12 or 14 percent earnings on $88 billion, “We start solving a lot of our financial problems really quick.”

“We gotta cut government. We gotta keep submitting, as the governor I’m just gonna tell you, knowing that the math isn’t there, the money’s not there, I’m gonna submit a full PFD because it has a little word in front of it, it’s called statutory. And if you stop asking for a full statutory PFD once, you’ll never get it ever again,” Bronson said.

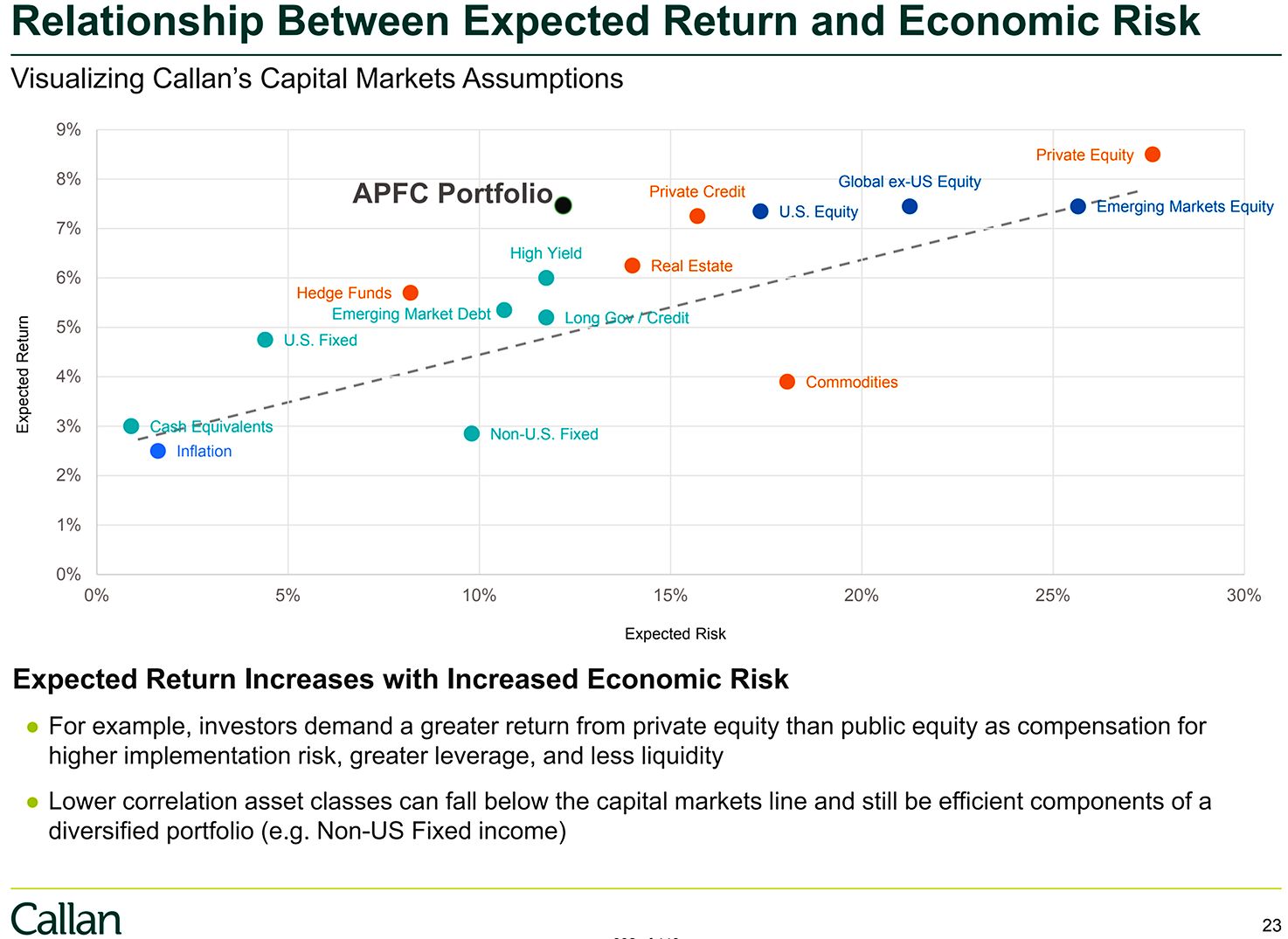

For a serious look at investment returns and what the target rate should be, let’s look at some information the fund recently received from Callan Associates, the Permanent Fund’s longtime general performance consultant.

In the Callan chart below see where the APFC investments now stand when economic risk and rewards are calculated. Then note that the 10 percent, or 12 percent or 14 percent Bronson target is way off the charts—meaning far more risk than even from private equity, where investors face higher returns and higher risks.

Your contributions help support independent analysis and political commentary by Alaska reporter and author Dermot Cole. Thank you for reading and for your support. Either click here to use PayPal or send checks to: Dermot Cole, Box 10673, Fairbanks, AK 99710-0673.\

Write me at dermotmcole@gmail.com

{kind=link}