Audit blasts Crum $225 million investment plan that ignored clear state procedures

Former Revenue Commissioner Adam Crum ignored numerous safeguards and pressed ahead with his decision to try to put $225 million into long-term investments last year, neglecting to follow the advice of the chief investment officer of the Department of Revenue and key legislators.

Legislative finance leaders wrote to Crum on May 19 that all money in the Constitutional Budget Reserve should have remained in cash or in investments that could be turned into cash quickly because the state could run short.

Crum signed a deal to put $75 million into a private infrastructure fund managed by DigitalBridge, an investment that made the money unavailable for at least five years. Only $50 million was transferred, however.

His replacement at the revenue department canceled the two other investments, each worth $75 million, after Crum was gone, limiting the damage.

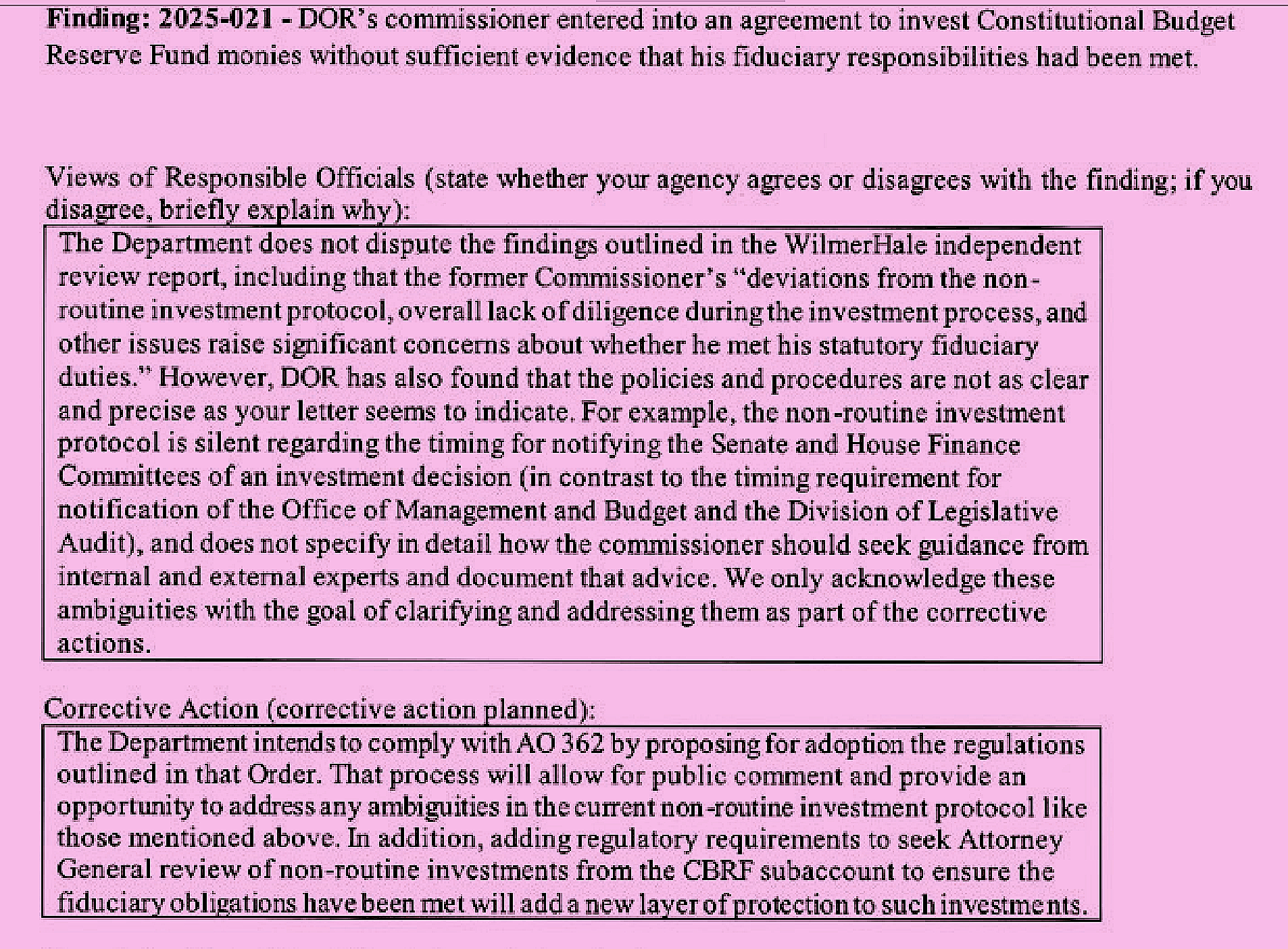

The Division of Legislative Audit concludes in its latest annual audit of state operations that Crum failed to follow seven investment procedures during his final days with the state, all related to documentation, investment guidance and disclosure.

The main reason for keeping the CBR entirely in cash is that the Dunleavy administration has no fiscal plan and the governor proposes massive deficits that would have to be covered by withdrawing $1 billion or $2 billion from the CBR each year.

Crum, who was supposedly supervised by Gov. Mike Dunleavy at the time, is one of the Republican candidates for governor, claiming that his financial and investment experience are his main strengths.

This incident alone should be enough to disqualify him from becoming governor because this is no way to manage the state’s cash.

The audit confirms the findings of a law firm hired to investigate Crum’s actions last fall.

No one who reads the audit and the law firm investigation and understands English can fairly reach that conclusion.

Here is Crum’s press release. In it he lies that the law firm investigation of Crum showed that “I did everything by the book.”

I have no clue what book Crum is talking about.

He may be hoping that no one reads the reports.

The law firm hired by Dunleavy concluded that “deviations from the non-routine investment protocol, overall lack of diligence during the investment process, and other issues raise significant concerns about whether he (Crum) met his statutory fiduciary duties.”

Janelle Earls, the acting revenue commissioner, told the auditors she “does not dispute the findings” in the report by WilmerHale, a backhanded way of agreeing that Crum displayed an “overall lack of diligence.”

The Dunleavy administration unloaded the Digital Bridge investment at a loss of $800,000. If you include the $350,000 that Dunleavy spent to investigate Crum and money that could have been earned with better short-term investments, the loss is well in excess of $1 million.

Crum had approved three investments of $75 million each, but two were incomplete before he quit.

On August 5, he ordered that $225 million be moved into a separate account and he sent a memo updating investment guidelines to allow private equity investments.

He told the Office of Management and Budget about his decision on August 7. He never informed the legislative leaders who had warned him in the spring that long-term investments should not be made with the budget reserve.

August 8 was his last day on the job.

The acting revenue commissioner who took over after Crum stopped two of the proposed investments, worth a total of $150 million, that had not been signed before he quit.

That left the $75 million DigitalBridge investment in “digital infrastructure” the only one standing.

Crum claimed his $225 million plan was about investing money to “bring together three world class infrastructure investors to bring financial returns and attention to the state of Alaska.”

Here is the full WilmerHale report.

The law firm has redacted the names of the other two companies. According to information that was not redacted, one of them appears to be Blackstone, the world’s largest alternative investment manager. The other company appears to be I Squared Capital, founded by Morgan Stanley executives in 2012.

Crum and Dunleavy have yet to be held accountable for the reckless and incompetent decision to put money that could be needed immediately into long-term investments where it could only be cashed in at a loss.

“The commissioner’s failure to follow DOR’s investment procedures calls into question compliance with CBRF (Constitutional Budget Reserve Fund) fiduciary responsibilities,” the auditors said, a polite way of saying there are serious questions of ethics and judgement.

“It is unclear why the commissioner did not follow DOR non-routine investment procedures. A lack of formal oversight of the DOR commissioner’s investment functions contributed to the noted deficiencies,” the audit found.

The “lack of formal oversight” means that for whatever reason, Dunleavy wasn’t doing his job, which is to supervise his commissioners.

The regulation changes that Dunleavy is now proposing to prevent another incident like this are only necessary because of failures by the former revenue commissioner and the current governor.

Crum claimed that because the WilmerHale report did not find that a state law had been violated that what he did was appropriate.

This was never about potential criminal violations. It was about judgement and making sound decisions with public funds. On that score, the law firm’s report and the new state audit leave no doubt that Crum was wrong.

Your contributions help support independent analysis and political commentary by Alaska reporter and author Dermot Cole. Thank you for reading and for your support. Either click here to use PayPal or send checks to: Dermot Cole, Box 10673, Fairbanks, AK 99710-0673.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}