Report whitewashes governor's role in approving Crum's $225M scheme

The law firm hired by the Dunleavy administration goes to great lengths to absolve Gov. Mike Dunleavy and his staff for failing to stop Adam Crum’s scheme to take $225 million from the Constitutional Budget Reserve and make long-term investments with it.

The administration paid $350,000 to an Outside law firm and received a report that blames the entire episode on Crum, portraying the governor and his staff as innocents.

I’m afraid the coverage of this report on my blog and that in the Anchorage Daily News has been a bit muddled.

A big reason for that is that the report is a bit muddled, paying too much attention to the bureaucratic process and not enough to the policy error.

The big thing to know is this: The entire Constitutional Budget Reserve should be kept in cash because it could be needed to pay day-to-day expenses of the state.

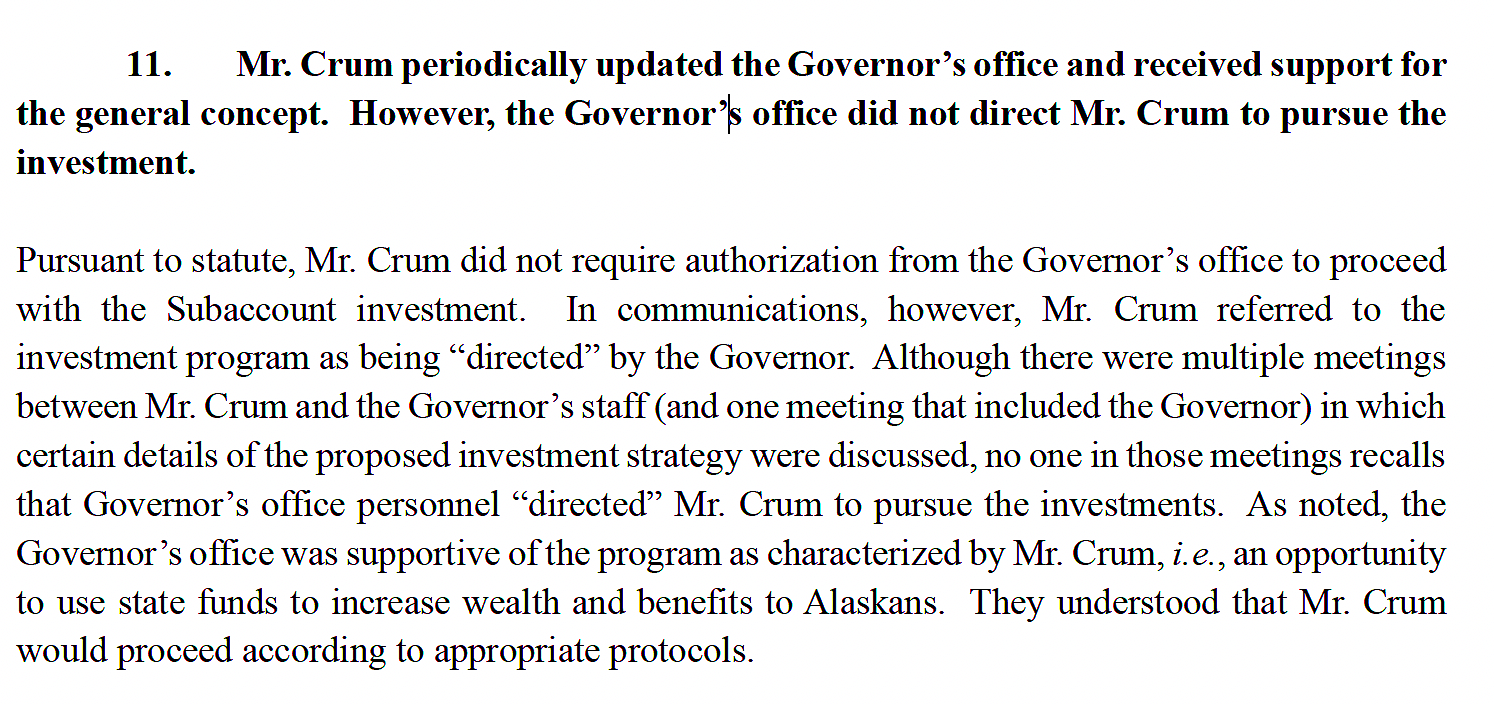

But Dunleavy and his staff signed onto the “general concept” of putting $225 million into long-term investments that could not easily be turned into cash.

In June 2025, Crum gave a document to Dunleavy and his staff about a plan to invest CBR funds “in private infrastructure funds that would pay higher returns” than keeping the money in cash.

These funds have much higher risks than “cash equivalents” such as short-term government bonds and they cannot be turned into cash immediately without paying penalties.

A competent governor and his staff would have ordered Crum to stop. Crum was out of his depth as revenue commissioner.

Dunleavy named him health commissioner in 2018 and revenue commissioner in 2022. His only real qualification to be revenue commissioner was his allegiance to Dunleavy.

On May 19 last year the leaders of the Senate Finance Committee warned Crum about keeping the entire budget reserve in cash to balance the state budget for this fiscal year and the next fiscal year.

Crum misled legislators in a June 27 reply by attaching a document showing that the fund’s investment plan was 100 percent cash. He hid from them that he was in the process of changing the fund’s investment goals to allow $225 million in long-term investments in “infrastructure funds” that could not be easily turned into cash.

Crum’s misleading letter was copied to the governor’s office and the Office of Management and Budget.

He also submitted a document claiming that the long-term investment was needed to deal with an “over-reliance on interest rates.” That makes absolutely no sense.

The state has sold the investment that Crum signed before he quit his state job at a loss that exceeds $1 million, including the $350,000 wasted on the report to find out what happened.

I agree with Sen. Bert Stedman, who told the Daily News that this was not about criminal activity, but gross incompetence.

Your contributions help support independent analysis and political commentary by Alaska reporter and author Dermot Cole. Thank you for reading and for your support. Either click here to use PayPal or send checks to: Dermot Cole, Box 10673, Fairbanks, AK 99710-0673.

In a marvel of double talk, the law firm says the governor’s office approved the “general concept” of Crum’s plan to move $225 million of short-term money into long-term investments.