Drop the pretense state never examined impact of cutting oil tax credits

Anchorage Sen. Forrest Dunbar asked a good question during a meeting of the Senate Resources Committee Wednesday about whether Alaska has really studied the impact of the $8 per barrel tax credits on the level of oil production.

He asked if we know whether the credits work and if production would go up or down if the credits were increased or decreased.

Dan Stickel, chief economist in the revenue department, said the department doesn’t know and can’t say.

“It is extremely difficult, if not impossible, to predict with certainty how taxpayers will respond to a tax change,” said Stickel.

He said “an increase or decrease in the per taxable barrel credit would be expected to influence decision making, but we do not attempt to predict exactly how much that will impact investment or production.”

Dunbar replied that his question was probably 12 years too late, referring to the creation of the credit scheme with the passage of SB 21 in 2013.

“Why would we do this unless we were incentivizing and we had some sense of the level of the incentive? But I understand what Mr. Stickel said, it’s very complicated. On the other hand, we’ve talking about hundreds of millions of dollars,” he said.

With the passage of SB 21, Gov. Sean Parnell and his allies said the $8 per barrel credit would lead to increased oil production.

The tax break it creates is on the legacy oil fields that did not qualify for “new oil” incentives, but where costs are lower and facilities have long been in place.

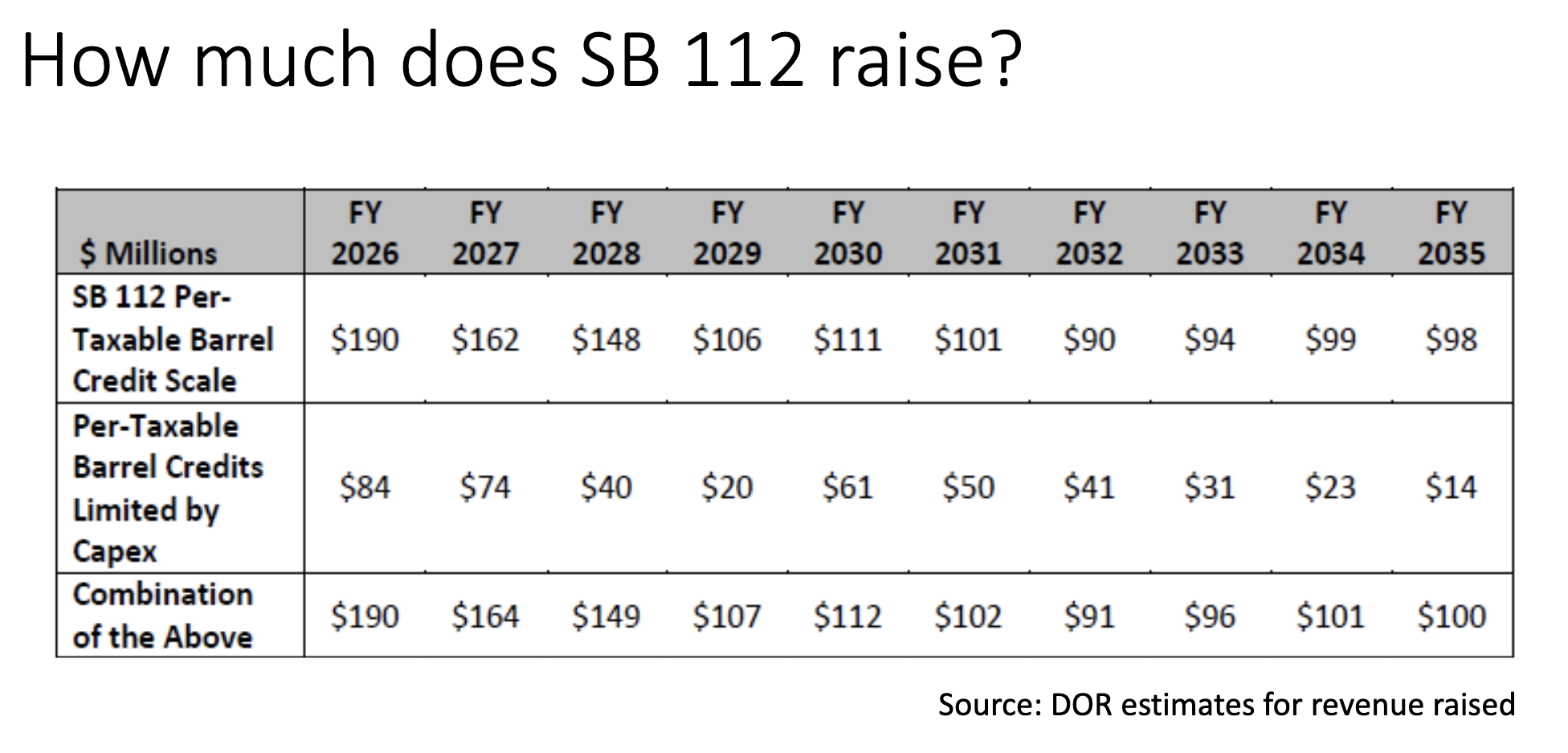

Dunbar’s question and Stickel’s answer came up during a discussion of Sen. Bill Wielechowski’s SB 112 to reduce the per barrel tax credit from a maximum of $8 to $5 per barrel.

This bill is one step toward erasing the state deficit and providing the money needed to adequately fund public education.

The Dunleavy revenue department is now hiding behind the statement that it is impossible to predict the future when tax law changes are proposed.

It’s true that no one can predict the future.

What is possible, however, is to rely upon people with expertise to analyze what is likely to happen.

In 2021, the revenue department studied what a reduction in the per barrel tax credit would probably mean. The department, then headed by Lucinda Mahoney, settled on a proposal to reduce the maximum credit to $5, comparable to Wielechowski’s bill.

At a Senate Finance hearing on January 28, 2022, former Deputy Revenue Commissioner Brian Fechter testified that the department had analyzed credit changes the previous summer and found that a reduction in credits would be justified.

At Wednesday’s meeting, Sen. Shelley Hughes, who hasn’t looked into this matter, concluded that there was no real analysis of tax credit reductions in 2021.

She said it “sounds like there wasn’t anything written or published or any actual modeling or analysis done by DOR, that was just a statement that he (Fechter) said, but we don’t have any backup documentation to that. And if we do, can you provide it to the committee?” she asked Stickel.

“I am not prepared to speak to the statements that the folks in the prior iteration of the commissioner’s office made. Department of Revenue has done a lot of analysis over the years, we have engaged consultants on and off. But I don’t know exactly what Deputy Commissioner Fechter was looking to when he made that statement,” Stickel said.

Hughes asked if Stickel could testify that oil production will not drop if tax credits are reduced.

“Can you say with confidence that this would not impact production revenue royaltites?”

“No, I would not say that with certainty,” he said.

Never has there been a more obvious question and answer.

Stickel can’t say anything with certainty. Better to make informed decisions with the best information available, realizing nothing is certain.

In August 2021, Sen. Jesse Kiehl asked Mahoney for details on how a tax credit reduction might change state revenue at different oil prices.

“We developed that as a part of our analysis in selecting $5 . So we will send that to you. Additionally we evaluated the government take component and the impact to profitability. So all of that was done. And we will send it your way,” Mahoney said.

This was at the time when Mahoney told legislators that Gov. Mike Dunleavy said that he would support the reduction of tax credits if the Legislature did.

These credits are now running at about $600 million a year.

Some of the analysis that Hughes said never took place and that Stickel said he was not prepared to talk about was contained in an October 1, 2021 letter from Mahoney to the legislative fiscal plan working group.

While Mahoney’s letter contains the usual “no one can predict the future” disclaimer, it also looks at the profits from North Slope oil at different prices if the credits are reduced.

“As the charts indicate, a 3-7% change in government take is seen at oil prices of $60 per barrel and above,” Mahoney said.

At $80 per barrel, the oil company share of profits would drop from 49 percent to 45 percent.

This was the research the Dunleavy administration relied upon to propose that a reduction in tax credits to $5 was warranted, if the Legislature approved it first. This is a minor tax increase. The oil industry will squeal, as it always does, certain that the sky is falling.

The Senate Resources Committee should call upon the Department of Revenue to elaborate on this analysis and drop the pretense that it doesn’t exist.

The charts below, taken from Mahoney’s letter, estimate the change in industry profits and government take under the current maximum of $8 a barrel and a proposal for a reduction to $5 a barrel.

There’s a lot more to say about this.

Your contributions help support independent analysis and political commentary by Alaska reporter and author Dermot Cole. Thank you for reading and for your support. Either click here to use PayPal or send checks to: Dermot Cole, Box 10673, Fairbanks, AK 99710-0673.